India’s power infrastructure is entering a once-in-a-decade expansion phase—and smart capital is already flowing into companies aligned with this theme.

Indo SMC is emerging as one of the most interesting plays in the unlisted space, backed by strong fundamentals, execution visibility, and a rapidly expanding order book.

Let’s break down the story with data, clarity, and investor-focused insights.

⚡ Macro Tailwind: Power Sector Growth

Market Growth Snapshot

| Segment | Current Size | Future Size | CAGR |

|---|---|---|---|

| Transformer Market | $26.68 B (2024) | $48.10 B (2034) | 6.07% |

| SMC Market | $1.72 B (2025) | $2.52 B (2034) | 4.36% |

| FRP Market | $79.06 B (2025) | $102.01 B (2030) | 5.23% |

📈 Growth Drivers

- Renewable energy expansion

- EV charging infrastructure

- Smart grids & urbanization

- Government electrification programs

👉 Indo SMC sits directly in the middle of all these trends.

Q3 FY26 Performance: A Clear Turning Point

Financial Snapshot

| Metric | Q3 FY26 |

|---|---|

| Revenue | ₹101.49 Cr |

| EBITDA | ₹16.45 Cr |

| PAT | ₹12.10 Cr |

| PAT Margin | ~11% |

Profitability Trend (Visual)

Q3 FY26 : ███████████ (~11%)

Target FY27 : ████████████ (12%+)

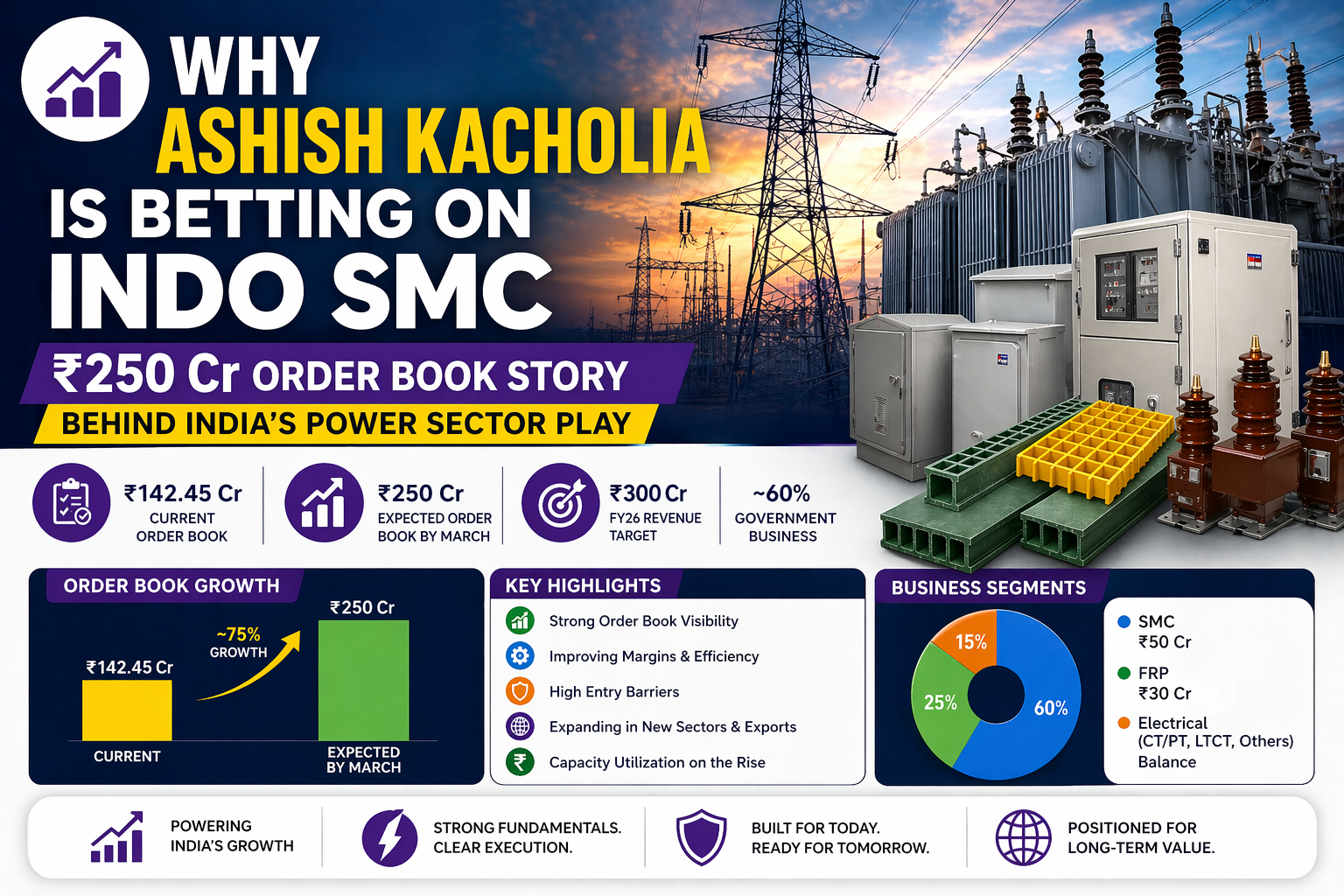

Real Trigger: Order Book Expansion

Order Book Evolution

| Timeline | Order Book |

|---|---|

| Current | ₹142.45 Cr |

| Expected (Mar) | ₹250 Cr |

Growth Visualization

₹200 Cr | ████████████████████

₹150 Cr | ██████████████

₹100 Cr | █████████

—————————

Order Book Mix

| Segment | Value |

|---|---|

| SMC | ₹50 Cr |

| FRP | ₹30 Cr |

| Electrical (CT/PT, LTCT) | Balance |

Why Order Book Matters More Than Revenue

| Metric | Meaning |

|---|---|

| Revenue | Past performance |

| Order Book | Future earnings visibility |

👉 A ₹250 Cr order book = predictable growth runway

Working Capital: Silent Game Changer

Receivable Days Improvement

| Period | Days |

|---|---|

| H1 FY26 | ~83 days |

| Q3 FY26 | ~40–45 days |

📉 Visual Drop

60 | ████████████

45 | ████████

———————–

H1 FY26 Q3 FY26

Business Mix & Growth Strategy

Revenue Mix

| Segment Type | Share |

|---|---|

| Government | ~60% |

| Private | ~40% |

👉 Government = stability

👉 Private = growth potential

Expansion Opportunities

New Sectors Being Targeted

| Sector | Opportunity |

|---|---|

| Railways | Vande Bharat ecosystem |

| Defense | Infrastructure supply |

| Metro | FRP applications |

| Auto | SMC enclosures |

| Exports | Middle East, Africa, Europe |

Export Expansion (Early Signal)

| Stage | Status |

|---|---|

| First Shipment | Oman (FRP products) |

| Next Targets | Africa |

| Future Plan | Europe & UK |

Capacity Utilization: Operating Leverage Ahead

Utilization Growth

| Stage | Utilization |

|---|---|

| IPO Phase | 30–40% |

| Current | 60–80% |

| Potential | 90% |

📈 Visual

80% | ████████████████

60% | ████████████

40% | ████████

———————-

Past Current Future

Growth Targets: Clear Roadmap

Revenue Targets

| Year | Target |

|---|---|

| FY26 | ~₹300 Cr |

| FY27 | ~₹450 Cr |

Segment-wise FY27 Target

| Segment | Revenue Target |

|---|---|

| Electrical | ₹250 Cr |

| SMC | ₹120–150 Cr |

| FRP | ₹70–80 Cr |

Margin Strategy Breakdown

| Factor | Impact |

|---|---|

| Cost Auditing | Structural margin improvement |

| Procurement Power | Better pricing |

| Manufacturing Shift | Higher profitability |

| Commodity Pass-through | Risk reduction |

CAPEX Deployment

| Investment Area | Details |

|---|---|

| Press Machine | 2000-ton unit |

| Pultrusion | 2 installed, 3 planned |

| Lab Upgrade | Nashik facility |

| Total CAPEX | ~₹25 Cr |

Competitive Moat

| Barrier Type | Impact |

|---|---|

| Approvals | High entry barrier |

| Certifications | Quality control |

| Tender access | Limited players |

| Experience | 3–4 years entry lag |

Tender Dynamics

Vendor B: 25%

Vendor C: 15%

Risks to Track

| Risk | Explanation |

|---|---|

| Order Book Variability | ₹142 Cr vs ₹250 Cr projection |

| Seasonality | Monsoon impact |

| Commodity Risk | Copper fluctuations |

| Execution | New segments scaling |

Why Ashish Kacholia Is Betting Here

🔑 Investment Checklist

| Factor | Status |

|---|---|

| Order Visibility | ✅ Strong |

| Margin Expansion | ✅ Structural |

| Sector Tailwind | ✅ Strong |

| Entry Barriers | ✅ High |

| Growth Clarity | ✅ Defined |

| Export Optionality | ✅ Emerging |

Final Takeaway

Indo SMC is shaping up as a high-conviction infrastructure play with:

- Strong order book momentum

- Improving margins

- Expanding sector presence

- High entry barriers

The ₹250 crore order book isn’t just growth—it’s visibility, predictability, and scalability.

Conclusion

As India accelerates its power and infrastructure journey, companies like Indo SMC are quietly building the backbone of this transformation.

For investors tracking the unlisted space, this is not just another story—it’s a data-backed, execution-led opportunity.

And when seasoned investors like Ashish Kacholia start taking positions, it’s often an early signal—not the peak.