India’s infrastructure and power sector transformation is creating a new wave of industrial growth stories. As the country accelerates investments in smart grids, renewable energy, metro rail, EV infrastructure, and electricity distribution modernization, companies supplying critical electrical infrastructure products are entering a strong long-term growth cycle.

One company increasingly attracting investor attention is Indo SMC Limited.

Backed by:

- Strong order book growth

- Improving margins

- Utility-focused demand

- Export expansion

- Capacity scaling

- Infrastructure tailwinds

Indo SMC is now being discussed as one of the emerging SME infrastructure stories to watch. And with investor interest linked to Ashish Kacholia, the spotlight has intensified even further. This report brings together all the latest updates, financials, management commentary, industry data, risks, and growth triggers in one place for investors.

India’s Power Infrastructure Opportunity

India’s power infrastructure sector is entering a multi-decade expansion phase.

📊 Industry Growth Snapshot

| Industry | Current Market Size | Future Projection | CAGR |

| Transformer Market | $26.68B (2024) | $48.10B (2034) | 6.07% |

| FRP Market | $79.06B (2025) | $102.01B (2030) | 5.23% |

| SMC Market | $1.72B (2025) | $2.52B (2034) | 4.36% |

📈 India Infrastructure Drivers

Renewable Energy Expansion ████████████████████

Smart Grid Modernization ██████████████████

EV Infrastructure ███████████████

Metro & Railway Electrification ████████████████

Government Utility Spending ███████████████████

These trends are creating rising demand for:

- Metering cubicles

- CT/PT transformers

- SMC electrical products

- FRP industrial solutions

And Indo SMC is positioned directly inside these growth areas.

🏭 Indo SMC Business Overview

Indo SMC manufactures products used in:

- Electrical infrastructure

- Utilities

- Government projects

- Industrial facilities

- Transportation infrastructure

📦 Core Business Segments

| Segment | Products |

| SMC Products | Meter boxes, enclosures |

| FRP Products | Cable trays, gratings |

| Electrical Products | CT/PT, LTCT, metering cubicles |

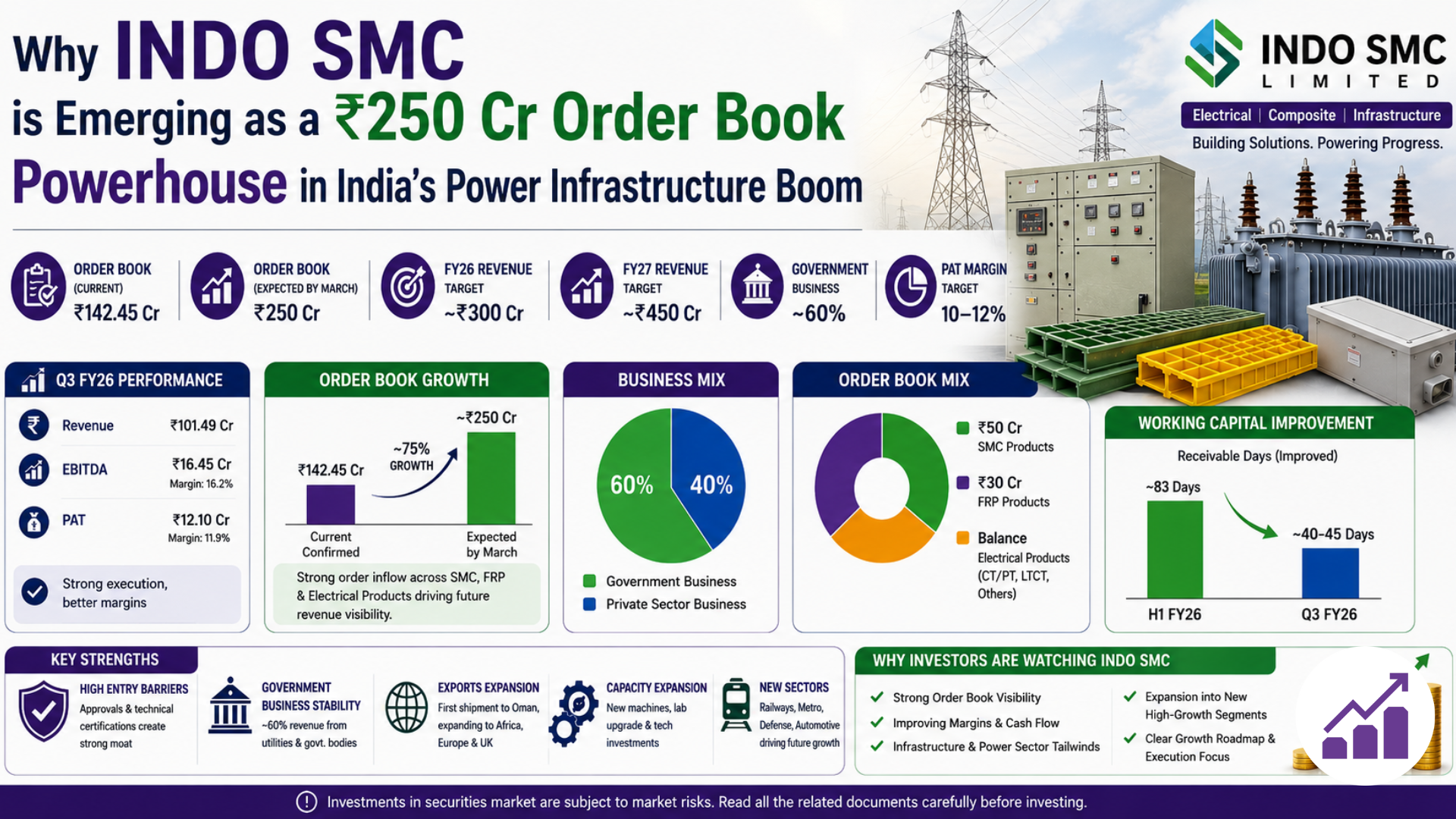

Q3 FY26: Quarter That Changed Market Attention

Indo SMC’s Q3 FY26 numbers became a major trigger for investor interest.

💰 Q3 FY26 Financial Performance

| Metric | Q3 FY26 |

| Revenue | ₹101.49 Cr |

| EBITDA | ₹16.45 Cr |

| PAT | ₹12.10 Cr |

| PAT Margin | ~11.9% |

📈 Profitability Trend

PAT Margin Progression

FY25 Average ████████ (~8-9%)

Q3 FY26 ████████████ (~11.9%)

Management Target █████████████ (12%+)

Management attributed improvement to:

- Operating leverage

- Cost optimization

- Better execution

- Manufacturing efficiencies

This is important because it indicates the business may be entering a more profitable operating phase.

📦 The ₹250 Cr Order Book Story

The biggest discussion point around Indo SMC currently is its order book.

📊 Order Book Snapshot

| Timeline | Order Book |

| Current Confirmed | ₹142.45 Cr |

| Expected by March | ~₹250 Cr |

📈 Order Book Growth Visualization

Order Book Growth

₹250 Cr | ██████████████████████████████

₹200 Cr | ██████████████████████

₹150 Cr | ███████████████

₹100 Cr | ██████████

That projected jump from ₹142 Cr to ₹250 Cr represents:

- Strong tender wins

- Demand visibility

- Future revenue pipeline

- Scaling confidence

🔍 Order Book Mix

| Segment | Approximate Contribution |

| SMC | ₹50 Cr |

| FRP | ₹30 Cr |

| Electrical Products | Remaining Balance |

This diversification reduces concentration risk while keeping the company exposed to multiple infrastructure themes.

💡 Why Investors Care About Order Books?

For infrastructure businesses:

| Metric | Meaning |

| Revenue | Past execution |

| Order Book | Future visibility |

A growing order book generally signals:

- Strong market positioning

- Execution capability

- Revenue predictability

This is one reason Indo SMC is gaining investor interest.

🚀 Revenue Growth Targets

Management has provided aggressive guidance for the coming years.

📊 Revenue Vision

| Year | Revenue Target |

| FY26 | ~₹300 Cr |

| FY27 | ~₹450 Cr |

📈 Revenue Growth Projection

Revenue Growth Potential

₹450 Cr | ██████████████████████████████

₹300 Cr | ███████████████████

₹150 Cr | ██████████

————————-

📊 Segment-Wise FY27 Ambition

| Segment | Revenue Target |

| Electrical Products | ₹250 Cr |

| SMC Products | ₹120–150 Cr |

| FRP Products | ₹70–80 Cr |

Management appears highly bullish on:

- SMC products

- CT/PT and LTCT electrical products

⚙️ Capacity Utilization Rising Rapidly

A major operational trigger is improving utilization.

📊 Utilization Levels

| Phase | Utilization |

| Earlier Phase | 30–40% |

| Current | 60–80% |

| Future Potential | Up to 90% |

📈 Operating Leverage Opportunity

Capacity Utilization

90% | ███████████████████████

80% | ██████████████████

60% | █████████████

40% | ████████

————————-

Higher utilization means:

- Better margins

- Lower per-unit costs

- Strong operating leverage

💰 Working Capital Transformation

One of the most underrated developments is the sharp improvement in receivables.

📊 Receivable Days

| Period | Days |

| H1 FY26 | ~83 Days |

| Q3 FY26 | ~40–45 Days |

📉 Working Capital Improvement

Receivable Days Reduction

90 Days | ██████████████████████

60 Days | █████████████

45 Days | ████████

———————

This improvement suggests:

- Better collections

- Faster cash conversion

- Improved liquidity

- Stronger financial discipline

🌍 Export Expansion Has Started

Exports are now becoming part of Indo SMC’s growth narrative.

Export Updates

| Development | Status |

| First Export Shipment | Oman |

| Export Products | FRP products |

| Next Focus Markets | Africa |

| Future Plans | Europe & UK |

Exported Products Include:

- FRP gratings

- Cable trays

- Pultrusion profiles

Exports can become:

- Margin accretive

- Revenue diversifying

- Scale enhancing

🚄 New Sector Expansion

Indo SMC is expanding beyond utility infrastructure.

📊 Emerging Opportunity Areas

| Sector | Opportunity |

| Railways | Vande Bharat ecosystem |

| Metro Projects | FRP infrastructure |

| Defense | Industrial infrastructure |

| Automotive | SMC enclosures |

Management has also indicated progress toward railway approvals.

🏗️ IPO CAPEX Deployment

The company is actively deploying IPO proceeds.

📊 Key Expansion Projects

| Investment | Purpose |

| 2000-ton Press | Production scaling |

| Pultrusion Machines | FRP expansion |

| Nashik Lab Upgrade | Technical approvals |

| Manufacturing Upgrades | Capacity enhancement |

📈 Margin Expansion Story

Management believes margin improvement is structural.

📊 Margin Drivers

| Factor | Impact |

| Cost Auditing | Better profitability |

| Procurement Scale | Improved pricing |

| Manufacturing Shift | Higher margins |

| Commodity Pass-Through | Lower volatility |

🎯 Margin Target

| Metric | Target |

| PAT Margin | 10–12% |

Q3 FY26 has already reached:

- ~11.9% PAT margin

🔐 Strong Entry Barriers

Indo SMC operates in a highly approval-driven industry.

Competitive Advantages

| Barrier | Impact |

| Utility Approvals | Limits competition |

| Vendor Registrations | Tender eligibility |

| Technical Certifications | Quality moat |

| Industry Experience | Long onboarding time |

Management claims new entrants may require:

- 3–4 years to establish comparable approvals

This creates:

- Customer stickiness

- Competitive advantage

- Tender visibility

🧾 Government Business Adds Stability

Approximately:

- 60% of revenue comes from government-linked business

Including:

- DISCOMs

- State Electricity Boards

- Utility tenders

📊 Revenue Mix

Government Business ████████████████ 60%

Private Sector ██████████ 40%

Government business provides:

- Stable demand

- Long-term infrastructure visibility

- Lower default risk

⚠️ Risks Investors Should Track

No growth story is risk-free.

Key Risks

| Risk | Explanation |

| Order Execution | Large order conversion needed |

| Commodity Prices | Copper & raw material volatility |

| Seasonality | Monsoon impacts production |

| Expansion Risks | Railway/export scaling |

However, management says commodity fluctuations are increasingly pass-through-based.

Why Are Investors Watching Indo SMC Closely?

Indo SMC now combines several investor-favorite themes:

✅ Infrastructure growth

✅ Power sector exposure

✅ Government demands stability

✅ Export opportunity

✅ Margin expansion

✅ Order book visibility

✅ Manufacturing scale-up

✅ Entry barriers

It fits the profile of companies often associated with long-term infrastructure compounding stories.

Final Thoughts

Indo SMC is gradually evolving from a small manufacturing business into a broader infrastructure-focused industrial platform.

Its current investment narrative revolves around:

- ₹250 Cr order book visibility

- Improving profitability

- Export expansion

- Utility infrastructure demand

- Capacity scaling

- Power sector tailwinds

Most importantly, the company is operating in sectors where India’s long-term capital expenditure cycle is only beginning.

India’s infrastructure and power transformation is creating opportunities for specialized manufacturing companies capable of scaling efficiently.

Indo SMC’s combination of:

- Strong order visibility

- Improving margins

- Export potential

- Government-linked business

- Expansion into new sectors

is now making it one of the more closely watched SME infrastructure stories among investors.

If management successfully executes its ₹250 crore order book roadmap and FY27 growth plans, Indo SMC could emerge as a significant player in India’s evolving electrical infrastructure ecosystem.

FAQs: Indo SMC Limited

What does Indo SMC Limited do?

Indo SMC Limited manufactures electrical and composite infrastructure products used in power distribution, utilities, industrial infrastructure, railways, and metro projects.

Its key product categories include:

- SMC meter boxes and enclosures

- FRP cable trays and gratings

- CT/PT transformers

- LTCT and metering cubicles

Why is Indo SMC gaining investor attention?

Indo SMC is attracting investor interest because of:

- Strong Q3 FY26 financial performance

- Rapidly growing order book

- Expansion into exports and railways

- Improving margins

- Government-linked business stability

- Exposure to India’s power infrastructure growth

The company’s expected ₹250 crore order book has become one of the key discussion points among investors.

What is Indo SMC’s current order book?

Management stated that:

- Current confirmed order book is around ₹142.45 crore

- The company expects the order book to reach approximately ₹250 crore by March

This provides strong future revenue visibility.

What were Indo SMC’s Q3 FY26 results?

Q3 FY26 Performance Snapshot

| Metric | Q3 FY26 |

| Revenue | ₹101.49 Cr |

| EBITDA | ₹16.45 Cr |

| PAT | ₹12.10 Cr |

| PAT Margin | ~11.9% |

Management attributed the growth to operating leverage and disciplined cost management.

What are Indo SMC’s growth targets?

Management has indicated:

- FY26 revenue target: ~₹300 crore

- FY27 revenue target: ~₹450 crore

The company is targeting growth across:

- Electrical products

- SMC products

- FRP solutions

What industries does Indo SMC serve?

Indo SMC serves multiple sectors including:

- Power utilities

- Electrical infrastructure

- Railways

- Metro projects

- Defense

- Industrial infrastructure

- Automotive applications

Is Indo SMC involved in exports?

Yes.

The company recently shipped its first export container to Oman.

Exported products include:

- FRP gratings

- Cable trays

- Pultrusion products

Management has also mentioned expansion plans into:

- Africa

- Europe

- UK markets

Why is the order book important for Indo SMC?

For infrastructure and manufacturing businesses, order books indicate:

- Future revenue visibility

- Demand strength

- Production planning confidence

- Business scalability

A rising order book is generally considered a positive signal by investors.

What is Indo SMC’s business mix?

Approximately:

- 60% of revenue comes from government-linked business

- 40% comes from private sector business

Government business includes:

- DISCOMs

- State Electricity Boards

- Utility infrastructure projects

What are Indo SMC’s key competitive advantages?

Some major strengths include:

- Utility approvals

- Vendor registrations

- Technical certifications

- Diversified product portfolio

- High entry barriers

- Government infrastructure exposure

Management claims new entrants may require 3–4 years to build similar approvals.

What are Indo SMC’s margin targets?

Management has indicated:

- PAT margin target range of 10–12%

The company believes margin improvements are structural due to:

- Better procurement

- Cost auditing systems

- Manufacturing efficiencies

- Commodity pass-through pricing

Has Indo SMC improved working capital efficiency?

Yes.

Receivable days reportedly improved from:

- ~83 days in H1 FY26

to - ~40–45 days in Q3 FY26

This suggests:

- Faster collections

- Better cash flow management

- Improved financial discipline

What CAPEX expansion is Indo SMC undertaking?

The company is deploying IPO proceeds toward:

- 2000-ton press machine

- Pultrusion machines

- Laboratory upgrades

- Manufacturing expansion

These investments are aimed at scaling production and supporting future approvals.

Is Indo SMC connected to India’s power infrastructure growth story?

Yes.

Indo SMC operates in sectors benefiting from:

- Grid modernization

- Renewable energy expansion

- Smart meter deployment

- Railway electrification

- EV infrastructure growth

This places the company within long-term infrastructure spending themes in India.

What risks should investors monitor in Indo SMC?

Key risks include:

- Execution of projected order book

- Commodity price fluctuations

- Seasonal production disruptions

- Export expansion risks

- Dependence on approvals and tenders

Investors should monitor whether management delivers on its growth and margin guidance.

Why is Ashish Kacholia linked with Indo SMC discussions?

Ashish Kacholia is known for identifying scalable growth businesses early.

Indo SMC is being discussed in investor circles because it fits several themes often associated with growth-focused investing:

- Infrastructure exposure

- Manufacturing scale-up

- Improving profitability

- Strong order visibility

- Sector tailwinds

What makes Indo SMC different from typical SME manufacturing companies?

Unlike many SME manufacturers, Indo SMC operates in:

- Approval-driven markets

- Utility infrastructure

- Specialized electrical systems

Its business requires:

- Technical certifications

- Vendor approvals

- Product compliance

These create stronger entry barriers compared to generic manufacturing businesses.

What should investors watch next for Indo SMC?

Important upcoming triggers include:

- Whether order book reaches ₹250 crore

- FY26 revenue execution

- Margin sustainability

- Export growth

- Railway approvals

- Capacity utilization improvements

These factors may shape future investor sentiment around the company.